Gift Letter for Mortgage Guide and Sample for Homebuyer

Majority of people that plan to be a homeowner often feel burden of massive payment and to pay off the borrowed money over future years ahead. It can be a daunting task, so they would probably turn use generous gift of cash to secure their mortgage few months in advance. If you are included in this category, it is possible to still not understand clearly how to take the case and specifically utilize it to cover the mortgage payments or cover the down payment. To convince the lenders that the cash is a valid gift to pay the moneylending and not another loan, you will need to send gift letter for mortgage.

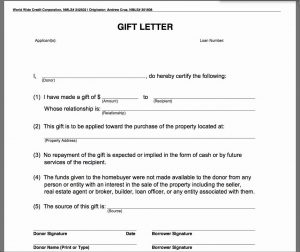

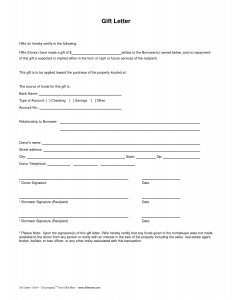

What Is Gift Letter?

Gift letter for mortgage is the note that used to explain that the money you use for payment is from a donor and you do not have to pay the donor money back. The donor has to write the letter to make sure that the money used as part or whole down payment is a gift instead of another loan. For example, your grandma saved some money to you the day that you decided to buy the first property, or your wedding money gift to wish you a happy and long marriage, or presents from your parents in form of fund to help you take huge burden of paying the home purchasing process.

What Are the Letter Requirements?

The gift letter for mortgage doesn’t have to be lengthy or complex; instead it should integrate some key points. The most important thing to remember is that it should be written by the approved donor who gives the fund. Here are some things need to be included inside.

- Gift amount

Make sure you write down the exact amount of money that the donor is giving you.

- Date of gift

Write down the date (MM/DD/YY) that the fund was given to you or transferred to the account under your name.

- The donor’s information

Write your donor identity such as the name, address, contact or phone number, and how are you related to the donor.

- Gift statement

To make it clear that the donor doesn’t expect repayment back, have the donor write the statement about it.

- Donor’s signature

As any other legal documents, it needs to be signed. In this case, the donor has to sign the letter along with name.

- Address of purchased home (optional)

It is not always required, but just in case the mortgage requested it, then write down your purchased home’s address.

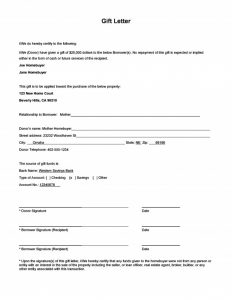

Sample of Gift Mortgage

In case your lender doesn’t have specific preferred gift letter for mortgage format, use the example below to write it:

October 15, 2019

To whom it may concern,

I am, the mother of Anna Smith, is giving my daughter, a gift of $10,000 to use as fund to purchase her home. I do not require or expect any kind of repayment. I wrote down the fund’s check on October 10, 2019 and she deposited it two days later. Regarding to this contribution, if you ever need to contact me, please do so by contacting (contact number).

Sincerely,

Johanna Smith

831 West Main Street

San Fransisco, CA 24018

(123) 456-7890

What to Do After You Send It?

Be in touch with the mortgage company, because they might ask for fund transfer documentation, like the deposit slip from your account or the donor’s check copy. This is intended to prove that the money source is not another lender and that you are not taking another debt.

If you are going to be the payment donor or the homebuyer, and going to use gift as the down payment, it is always possible to ask help from professional about the best option, or contact the lender to consult or learn about the gift letter for mortgage.

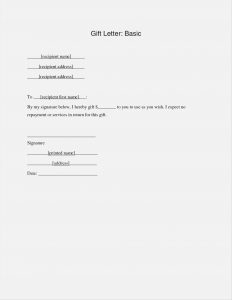

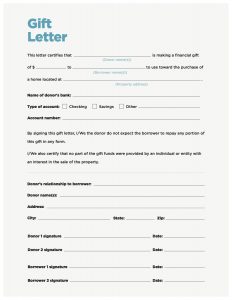

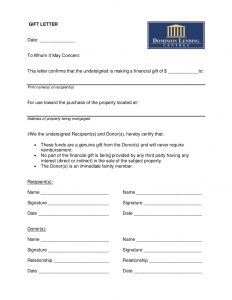

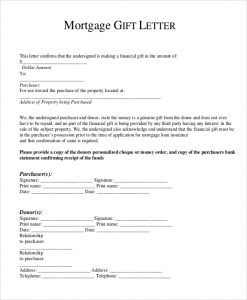

gift letter for mortgage

gift letter for mortgage

gift letter for mortgage

gift letter for mortgage

Please inform your expert on the intent of the debt if you expect to have a large amount of money to cover everything in your first payment. Providing is an important one. It can not be easy to provide an application to help or injure your request. A home can be offered as a gift for friendship. If a donation is a free gift, the mortgage will be violated due to one of the earliest loans.If you choose to use a gift for sale, it is important to remember the conditions and requirements.

The gift must be included in your account that can be recorded and that the library will integrate the money outlined in the free notebook to avoid potential problems. Also, you’d like to talk about the gift with your CPA or the mediator. Generally, there are some gifts to make if you are in a relationship. Of course, not all people are about a gift. However, if you have a real estate reward for earning it, you must keep the rules. Providing a reasonable amount of money for home improvement, there is an appropriate way to place a gift on your loan to continue caring for your customer. Of course, you can get a long-term reward for homemaking.

The FHA and the real estate loan schemes use financial funds for profit. If you are looking for a mortgage when buying your home, the payment can be paid. Those who pay the water are the ones who pay their mortgage more than their property, so they can ask the person who gives them something to think about a purchase. at least one, where the house was purchased for more money than money. . Once you have a prioritization, you need to consult a real estate agent to help you with the value of home sales. To compare HSBC’s moods, create the mood to meet your demands. Real estate risk must be understood by the simplicity of mobility and demanding more than you can. You can also afford financial assistance to help us by providing the right amount to buy with a real estate.

Because of failure, your application will be denied, and it can damage the future. An appropriate commentary on the amount of money financing in the trading business before the end of a home. While it is important to note such feedback ideas as a gift letter, it can be a donor and financial guarantee. The giver must be responsible for saving money on the paper. It must be an exclusive trademark.

Above all, the letter must indicate the actual amount given. In the end, you need to understand exactly what the applicants are asking for. You need to respond in writing within 14 days or to interrupt the help. So it’s a very good letter and needs to be written with care. You need to think about the gift cards. You need to receive the gift letter for your personal information and the amount of this time. You should also provide a gift voucher to the buyer to use a donation fund.

Evaluate our HSBC mortgages and determine which type of loan suits your needs. If you make an application for a mortgage when buying your next home, there may be a down payment. Submerged borrowers with more mortgage debt than homes are worth asking lenders to consider making a quick sale if the home is sold to another buyer for less. A joint mortgage should make it easier to get a mortgage and lend more than you would otherwise have.

If you receive the gift incorrectly, your lender will most likely disable your home loan program. If this gift is really a financial loan, you will be denied the mortgage due to lack of deposit funds. In order to be registered, it must be credited to your account and, in order to avoid any difficulty, the deposit must match the amount specified in this letter. When you receive your deposit, try to remember that there is the right way and the wrong method. Whenever you receive a cash gift for a down payment, there are easy ways to deposit the gift in your accounts to keep the lender happy.

You can choose not to violate the principles of receiving a gift. There is no limit to how much money a buyer can get as a gift gift. There is no particular need for how long gift money takes to maintain a home buyer’s bank accounts before the home closes. There are no special requirements for the duration of a Co-op reference game. The purpose of a cooperative gift correspondence is to provide the cooperative with written confirmation that any money you receive from others to finance a purchase is actually a gift, not a repayment loan. The giver should also keep a paper statement of money.

As a rule, gifts are only acceptable if they are outside of the family. For example, you cannot knowingly deposit your money into a bank account. Exactly, you can earn a last-minute cash gift for your home deposit.

For all purposes of this collaborative counseling program, it is usually ok that you submit a copy of the same cover letter that you use for the mortgage process. In order to use your existing capital, you must provide a regular letter to the lender.

This font must be grammatical and accurate. This letter should also include your contact information and the value of the gift. Again, the correspondence must be detailed and it must be everything you plan to do with the accumulated capital. In the end, it should tell you exactly what borrowers are looking for. First and foremost, reference letters must be comprehensible and concise. The letter of reference from the regular owner should include the address of the equipment you are renting, the total length of time spent there, and the contract number.

Gifts can be an important tool for people seeking to finance their very first house, and understanding how to correctly apply a mortgage gift to your down payment is important when you’re planning to get a gift of down payment. Evidently, not everybody has a relative that may give a present. First of all, a gift canhave no strings attached. What’s more, it’s highly advised to talk about the gift with your CPA or tax professional.

You’re able to mention the reason you liked the gift and the way it can actually be of use to your lifestyle. If you might have the gift handled in the upcoming few weeks that would be perfect. Make certain you know of the gift that the individual has given so you can write the proper gift that you’re thankful for. If you have made the decision to use a present for a purchase it’s important to bear in mind that there are rules and documentation requirements.

Writing a terrific Hardship Letter, has come to be one of the most significant measures in having a thriving short sale approach. Therefore the secret to a prosperous hardship letter is to maintain it to a single paragraph or to just use the banks form, should they have one. Furthermore, the letter must specifically state that the funds aren’t financing. It should also be signed and dated. You merely require a gift letter from them stating that this is true. Gift letters could possibly be utilized in a great deal of ways based on the sort of gift given. It can function as a thank-you letter for the gift which has been received during an occasion, it may also be a letter stating the info about a gift donation, and it could also have items associated with the documentation of mortgage gift.

Excellent relationships begin at the beginning. Regardless of what, the connection between the borrower and donor has to be disclosed. You should get upon the value of your request in a couple of short paragraphs. The aim of your letter is to demonstrate the bank which you don’t have money to put in the transaction or make the Monthly payments. So as to use a present toward purchasing a new home there are particular requirements you must fulfill. Although it’s important to comprehend gift requirements like the gift letter, who might be the donor, and verification of the funds.

Based on what you require money for you can even allow it to be profound and touching. So since you can tell, gift funds may aid a buyer get into a home in a huge way! If gift funds are deposited three or more months before the loan application, those monies are deemed seasoned funds and aren’t subject to FHA or Fannie Mae guidelines.

Instead, you can ask your lender to supply you with a mortgage gift letter template they’d love to use. The crucial thing is to apply with a lender that sees people who have a gift as a very low risk borrower. Your lender will allow you to document the paper trail. Every lender demands this. Some Australian lenders won’t lend to individuals who have received their deposit for a present. It is essential that they can determine that it is possible to pay the loan back. FHA has a number of the least restrictive rules regarding who might be a donor.

Similar Posts:

- Mortgage Gift Letter Template

- Sample Gift Letter

- Gift Letter Template

- Loan Agreement Template

- Personal Loan Contract

- Loan Promissory Note

- Personal Loan Agreement Pdf

- Loan Agreement Contract

- Gifting Letter Template

- Personal Loan Agreement Templates

- Sample Mortgage Note

- Loan Contract Template

- Simple Loan Agreement

- Loan Agreement Form

- Loan Agreement Pdf

- Simple Loan Agreement Pdf

- Promissory Note Template

- Personal Loan Contract Template

- Sample Loan Agreement

- Promissory Note Example

- Loan Payoff Letter

- Family Loan Agreement

- Sample Donation Request Letter For Non Profit

- Installment Payment Agreement Template

- Samples Hardship Letter

- Installment Payment Agreement

- Loan Agreement Sample

- Mortgage Note Sample

- Amortization Schedule Example

- Letter Of Hardship

- Sample Letter Asking For Donations For School

- Hardship Letter Sample

- Employees Loan Agreement

- Personal Loan Template

- Deposit Slip Templates

- Sample Promissory Note

- Payment Agreement Form

- Construction Draw Schedule

- Deposit Slips Example

- Loan Application Format

- Home Purchase Contract

- Deposit Slips Template

- Sample Thank You Letter For Donation Of Goods

- Mortgage Statement Template

- Real Estate Offer Letter

- Proof Of Income Letter

- Free Printable Promissory Note

- Free Promissory Note Template For Personal Loan

- Payment Agreement Letter Between Two Parties

- Proof Of Income

- Sample Nonprofit Gift Acknowledgement Letter

- Sample Bank Statement

- Sample Donation Thank You Letter

- Blank Promissory Note Form

- Promissory Note For Car

- Payment Plan Contract

- Free Promissory Note Template

- Payment Demand Letter

- Solicitation Letter Sample

- Letter Of Harship

- Gift Card Envelope Templates

- Sample Demand Letter For Payment Of Debt

- Sample Demand Letter For Payment

- Proof Of Income Self Employed

- Simple Promissory Note

- Printable Rent Receipt

- Promissory Note Templates Word

- Credit Application Form

- Payment Agreement Template

- Simple Promissory Note No Interest

- Fund Raising Letter Templates

- Sample Letter Asking For Donation

- Donation Letter Sample

- Deposit Receipt Template

- Late Rent Payment Letter